Global wood pellet market outlook for 2019

The trade in wood pellets in 2018 is estimated at 23.8 million tons, 26% higher than the 18.9 million tons in 2017. This article will look at the major markets in the coming years.

From the perspective of North American producers, 2018 is one of the best years for wood pellet trade for quite some time. With the rise of the British Drax power station, after several years of easing, new markets and consumers have driven strong growth in global demand. Imports from Denmark, South Korea and Japan were all at least 40% higher than before, and Japan’s imports of wood pellets more than doubled. After several years of weakness, better market conditions and less inventory have also led to strong growth in the heating market in North America and Europe.

United Kingdom

In 2018, with the commissioning of EPH’s 396 MW Lynemouth power station and the conversion of the fourth unit of the Drax power station, UK pellet demand increased significantly for the first time in a few years.

Looking ahead, growth will be driven primarily by the full operation of the Lynemouth power station and the increased availability of the Drax power station. By 2020, with the scheduled trial run of MGT’s 299 MW Teeside cogeneration plant, UK demand will increase again, with an estimated 1.5 million tons per year.

Netherlands

The Netherlands has a long history as a major market for industrial wood pellets. In 2010, the Netherlands was the largest market for industrial wood pellets – for co-firing to achieve renewable energy targets. After the introduction of the new renewable energy subsidy program in 2012, the market fell rapidly. The new SDE+ program calls for new sustainability standards to be established before biomass co-firing is eligible for subsidies. This sustainability standard was finally approved in 2015.

In 2016, four power stations received subsidies: RWE’s Amer and Eemshaven power stations, Engie Rotterdam and Uniper Maasvlakte 3 (MPP3). Unit 9 of Amer Power Station was co-fired under the old subsidy program, and a large amount of wood pellets were recovered in the fourth quarter of 2018.

Other power plants may start co-firing in 2019 and 2020, making the Netherlands once again the main market for industrial wood pellets. The increase in demand for co-firing in the Netherlands is expected to quickly approach 2.5 million tons.

Japan

Japan’s imports of wood pellets exceeded 1 million tons for the first time in 2018, about twice the amount imported in 2017. By the first three quarters of 2018, 63% of Japan’s wood chip imports came from Canada and 31% came from Vietnam. Because Japan supports fixed-price and long-term contracts for renewable energy feed-in tariffs, long-term contracts with strong rivals (such as Canada and the US) are the preferred method for most Japanese buyers to purchase wood pellets. We expect Japan’s wood pellet imports to continue to grow rapidly in the next few years, and imports are expected to exceed 5 million tons in 2023.

Korea

In South Korea, renewable energy is driven by the Renewable Energy Portfolio Standard (RPS), which requires utilities to get more and more energy from renewable sources. A tradable renewable energy certificate (REC) is used to demonstrate compliance. Utilities have three ways to satisfy RPS: to produce RECs themselves, to buy RECs on exchanges, or to pay a fine equivalent to 150% of the average REC price for the year. Utilities found that co-firing wood pellets is one of the most cost-effective ways to meet RPS.

However, due to the uncertainty of the value of RECs, electricity prices and particle prices, Korean buyers are more difficult to sign long-term contracts. Despite this, there are still successful contract negotiations with North American producers, especially with dedicated biomass power plants (rather than major utility companies co-firing at coal stations).

South Korea’s demand is mainly met by the rapid development of Southeast Asian wood chip production capacity. In 2018, South Korea’s imports of wood pellets are expected to reach 3.4 million tons, of which more than 95% are from Southeast Asia.

Pellet heating market

Although the industrial pellet market has received a lot of attention from market analysts, the heating market accounts for a large increase in global demand, and FutureMetrics forecasts strong growth in the next five years. Warm winters and low competitive fuel prices, especially heating oil, have slowed demand for pellet heating in North America and Europe over the past few years. Although the recent drop in oil prices has caused some concern, in most cases, pellets still save a lot of money compared to fossil fuels in Europe, and in addition to natural gas in the United States, North America does.

In most cases, the demand for pellet heating is provided by local producers and therefore has less impact on global trade. Although the United States, Germany, France, Austria, Sweden and other countries have a large demand for pellet heating, the only market that has a major impact on global trade is Italy, where pellets are mainly used for home heating. We estimate that Italy imported 2.3 million tons of pellets in 2018. The market may be bigger because there is a black market for Italian wood pellets to avoid a 22% VAT – estimated to be 200,000-300,000 tons provided by the Canadian Wood Chips Association.

The United States has one of the largest pellet heating markets in the world. The annual demand for 2018 is estimated to be 2.5 million to 3 million tons. Approximately 85% of US demand is met by small and medium-sized domestic producers, approximately 10% from Canada and 5% from industrial producers in the southern United States. In the past few years, the US pellet market has been overstocked, but it has been cleaned up. Manufacturers are now worried about the shortage of the 2018-2019 heating season, mainly due to fiber supply problems in the east (about 50% of the US market in the Northeast). We expect moderate growth in the US heating market in the next few years, but it is different from industrial market expectations.

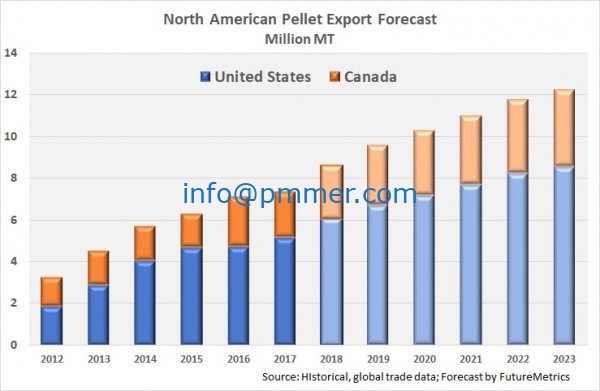

North American pellet production

North American grain exports will increase to the highest level in history in 2018. US pellet exports are expected to increase to 6.2 million tons, up 20% from 2017. Canadian grain exports are expected to increase to 2.4 million tons, an increase of 12.6% over the previous year. FutureMetrics estimates that US exports will increase to 8.5 million tons in 2023, while Canadian exports will increase to 3.7 million tons.

With the strong growth in pricing and demand in the industrial wood pellet market, we expect to develop new major industrial pellet mills in the southern United States after several years of real growth. In addition, the Pacific Northwest of the United States has the ability to supply a certain number of products to the fast-growing Asian pellet market. Maine is expected to become a new important export destination.

In western Canada, new growth is likely to be more pronounced. The loss of forest fires and the end of high harvest rates are affecting the production of sawmills, which affects the yield of the sawmill. Particle producers must purchase forest residues to maintain productivity. Several small and medium-sized industrial granulation plants will be seen in eastern Canada, as sawmills in these areas are looking for a market for surplus.